Tax season 2026 looks meaningfully different for both American and Canadian filers. In the US, the One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025 as Public Law 119-21, locked in the seven permanent federal income tax rates while expanding deductions and introducing new temporary exclusions. In Canada, the CRA applied a 2.0% federal indexing factor for January 1, 2026 and the lowest federal rate dropped to 14% following a reduction effective July 1, 2025. Whether you earn a paycheck in Chicago or Calgary, knowing exactly where your income lands on each country’s rate schedule is the first step toward minimizing your tax bill legally.

This guide draws on official IRS and CRA source documents to lay out every bracket, threshold, and notable deduction change for 2026. You will find a direct side-by-side comparison, analysis of who benefits most from the OBBBA changes, and a clear picture of what Canadian filers face under the newly indexed schedule. WideJournal’s personal finance guides and broader Finance articles cover these topics continuously as regulations evolve, so bookmark both resources for ongoing updates.

A word of caution before diving in: tax law is complex, thresholds interact with credits and deductions in non-obvious ways, and individual circumstances vary widely. The numbers below reflect official published figures as of May 2026, but your effective rate depends on your full financial picture. A qualified tax professional remains the most reliable resource for personal tax planning.

Key Takeaways

- The IRS confirmed seven permanent 2026 federal tax rates (10%, 12%, 22%, 24%, 32%, 35%, 37%) with the standard deduction rising to $16,100 for single filers and $32,200 for married filing jointly under the OBBBA.

- Canada’s lowest federal income tax rate is 14% for 2026 and subsequent years, following a mid-2025 rate reduction, with a 2.0% federal indexing factor applied to all 2026 bracket thresholds.

- The OBBBA’s no-tax-on-tips provision (2025 through 2028) and overtime deduction (up to $12,500 single / $25,000 joint) may meaningfully reduce taxable income for qualifying US workers.

- The US Child Tax Credit rises to $2,200 per qualifying child in 2026, while the maximum Earned Income Tax Credit reaches $8,231 under the updated IRS schedule.

- Canadian filers benefit from bracket indexation but face no equivalent to the OBBBA’s temporary deductions; higher earners above CAD $246,752 continue to pay a 33% federal marginal rate.

What Changed for US Filers Under the OBBBA?

The One Big Beautiful Bill Act made several 2017 tax cuts permanent while adding new temporary deductions, raising standard deductions significantly for 2026 and introducing exclusions for tip and overtime income.

The OBBBA’s most immediate impact for the average American filer is the enlarged standard deduction. According to the IRS announcement of 2026 tax inflation adjustments, the standard deduction for tax year 2026 is $16,100 for single filers, $32,200 for married couples filing jointly, and $24,200 for heads of household. These represent a notable jump from 2025 figures and reduce taxable income before a single deduction or credit is applied.

The IRS page on OBBBA provisions for individuals and workers confirms two temporary deductions worth watching. First, the no-tax-on-tips exclusion runs from 2025 through 2028, allowing qualifying service workers to exclude eligible tip income from federal income tax entirely. However, a critical nuance for workers to note is that this exclusion applies strictly to federal income tax; it does not exempt tip income from payroll taxes (FICA), meaning Social Security and Medicare withholdings will still be deducted as usual. Second, an overtime deduction allows eligible workers to deduct up to $12,500 in qualifying overtime pay ($25,000 for joint filers). Both provisions sunset after 2028 unless Congress acts, which introduces planning risk for workers who structure their earnings around those exclusions.

The estate tax exclusion climbs to $15 million per individual under the 2026 schedule, and the adoption credit rises to $17,670. The employer childcare credit was also expanded. Taken together, these shifts favor upper-middle and high-income households most, while the tip and overtime provisions target hourly and service-sector workers specifically.

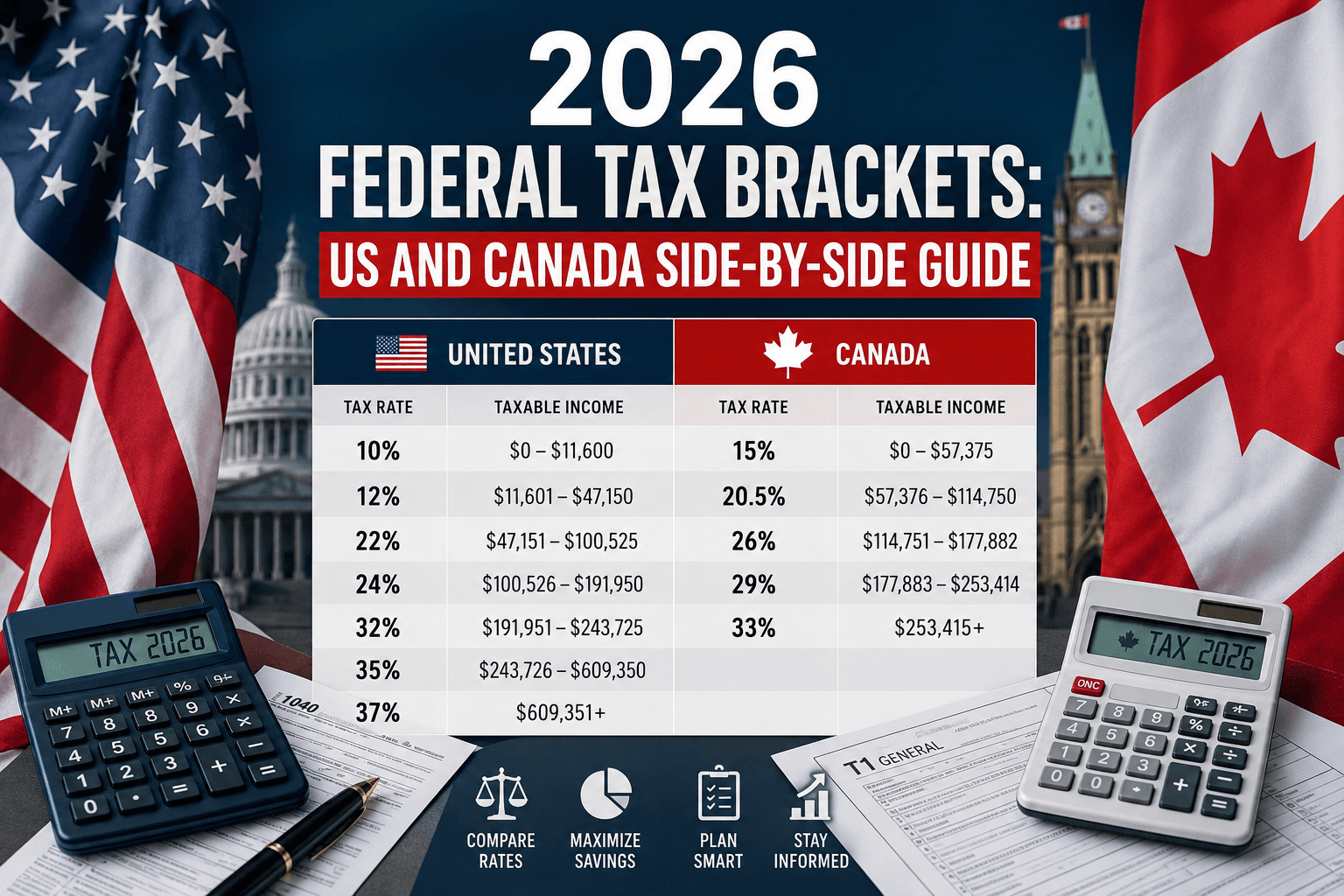

2026 US Federal Income Tax Brackets at a Glance

The Revenue Procedure 2025-32 confirms the seven-bracket structure. The thresholds below apply to single filers for tax year 2026:

| Rate | Taxable Income (Single) | Taxable Income (MFJ) |

|---|---|---|

| 10% | $0 to $11,925 | $0 to $23,850 |

| 12% | $11,926 to $48,475 | $23,851 to $96,950 |

| 22% | $48,476 to $103,350 | $96,951 to $206,700 |

| 24% | $103,351 to $197,300 | $206,701 to $394,600 |

| 32% | $197,301 to $250,525 | $394,601 to $501,050 |

| 35% | $250,526 to $626,350 | $501,051 to $751,600 |

| 37% | Over $626,350 | Over $751,600 |

Note that these thresholds apply to taxable income, meaning income after the standard deduction (or itemized deductions) has already reduced your gross income. A single filer earning $82,000 in wages does not land in the 22% bracket on the full amount; the first $16,100 is sheltered by the standard deduction, and only the income above each threshold is taxed at that bracket’s rate.

How Do Canada’s 2026 Federal Tax Brackets Compare?

Canada’s 2026 federal brackets are indexed at 2.0% and the lowest rate dropped to 14% following a July 2025 reduction, creating modest relief for lower-income filers while the top four rates remain unchanged.

Canadian federal income tax uses a five-bracket system. According to the CRA page on Canadian income tax rates for individuals, the rate reduction to the bottom bracket took effect July 1, 2025, bringing it from 15% to 14% for the 2026 tax year and beyond. The CRA T4032 Payroll Deductions Tables for January 2026 confirm the 14% rate and the 2.0% federal indexing factor applied to bracket thresholds from January 1, 2026.

| Rate | Federal Taxable Income (CAD) |

| 14% | $0 to $56,984 |

| 20.5% | $56,985 to $113,969 |

| 26% | $113,970 to $157,441 |

| 29% | $157,442 to $245,106 |

| 33% | Over $245,106 |

Official thresholds reflect the 2.0% indexation applied directly to the previous year’s base figures. Confirm your final numbers with your CRA notice of assessment or a payroll professional. Provincial and territorial taxes layer on top of federal rates, so a resident of Ontario or British Columbia faces a combined marginal rate considerably higher than the federal figure alone. Unlike the US system, Canada does not have a separate filing status multiplier for married couples at the federal level; individual income is taxed independently, though various credits apply to families.

US vs. Canada: Side-by-Side Comparison of Key Figures

Direct comparison reveals that the US OBBBA standard deduction represents a substantial up-front income shield, while Canada’s lower bottom rate provides targeted relief to lower-income earners without an equivalent broad deduction mechanism.

| Feature | United States (2026) | Canada (2026) |

|---|---|---|

| Bottom federal rate | 10% | 14% |

| Top federal rate | 37% | 33% |

| Number of brackets | 7 | 5 |

| Standard deduction (single) | $16,100 USD | Basic personal amount (~$16,129 CAD, indexed) |

| Child Tax Credit | $2,200 per child | Canada Child Benefit (income-tested, not a tax credit) |

| Bracket indexing | Inflation-adjusted annually (IRS) | 2.0% federal indexing factor (CRA, Jan 2026) |

| Notable 2026 change | OBBBA: tips/overtime deductions, higher standard deduction | Bottom rate cut from 15% to 14% (eff. July 1, 2025) |

For cross-border workers or dual citizens, the interaction between both systems can be complex. The US taxes citizens on worldwide income regardless of residence, while Canada taxes residents on their global earnings. To avoid paying tax twice on the same income, affected filers rely heavily on the US-Canada Tax Treaty, utilizing the Foreign Tax Credit (FTC) via IRS Form 1116 for US returns and CRA Form T2209 on the Canadian side. Those in this situation may benefit significantly from reviewing their position with a tax professional who specializes in cross-border planning. If higher-interest debt is consuming cash that could otherwise fund tax-advantaged accounts, exploring options like how to consolidate credit card debt may free up room to maximize RRSP or 401(k) contributions before the respective year-end deadlines.

Who Wins and Who Loses Under These 2026 Structures?

Lower-income American workers in tipped or overtime roles stand to benefit most from OBBBA’s temporary deductions, while high earners gain most from the permanently higher standard deduction and elevated estate exclusion.

For US filers, the math on the OBBBA changes is not evenly distributed. A restaurant server earning $35,000 in wages and $15,000 in tips may see a meaningful reduction in taxable income under the no-tax-on-tips exclusion, though the provision expires after 2028 and depends on qualifying conditions the IRS has outlined. A dual-income household where both spouses work overtime could shelter up to $25,000 in overtime pay, a benefit that disproportionately helps skilled trades and healthcare workers with frequent overtime schedules.

High earners benefit most from the permanently enlarged standard deduction and the $15 million estate exclusion. A married couple with $500,000 in combined income still pays a top marginal rate of 37% on income above $751,600, but the $32,200 standard deduction reduces the income subject to those rates from dollar one. The Child Tax Credit rising to $2,200 provides modest additional relief for families, though it phases out at higher income levels.

In Canada, the 1 percentage point reduction at the bottom rate translates to a maximum federal tax savings of roughly CAD $574 annually for anyone earning above the first bracket threshold. It helps lower-income earners most in absolute terms as a share of their tax bill, but the dollar amounts are modest. Middle and upper-income Canadian earners see little structural change in 2026 beyond the 2.0% indexation of brackets, which mainly prevents bracket creep from eroding real purchasing power.

12-Month Outlook: What Might Shift?

The OBBBA’s tip and overtime deductions sunset after 2028. Whether Congress renews them will likely become a legislative issue in 2027, and workers who have restructured compensation arrangements around those exclusions carry real planning risk if renewal stalls. On the Canadian side, the CRA’s indexation mechanism should continue at a rate reflecting inflation trends; if inflation cools further, the 2027 indexing factor may be lower than 2.0%, limiting future threshold growth. Both countries’ fiscal positions suggest limited appetite for broad rate reductions in the near term.

Alternative Perspectives

Some tax policy analysts argue that the OBBBA’s enlarged standard deduction, while broadly beneficial, reduces the incentive to itemize for middle-income filers who previously deducted mortgage interest or state and local taxes. Homeowners in high-tax states like California or New York may find their effective federal tax situation is less favorable than the headline numbers suggest because the $10,000 SALT cap remains in place, limiting itemized deductions for those who might otherwise exceed the standard deduction threshold.

On the Canadian side, critics of the bottom-rate reduction note that it was applied only from July 1, 2025, meaning the effective 2025 tax year benefit was roughly half of what a full-year cut would have delivered. For 2026, the full-year 14% rate applies, but some economists argue a broader structural reform to Canada’s five-bracket system would deliver more meaningful relief than incremental rate adjustments at the lower end.

“The IRS has released tax inflation adjustments for tax year 2026, including changes from the One, Big, Beautiful Bill signed into law on July 4, 2025.” — IRS Newsroom, 2025“The federal indexing factor for January 1, 2026 is 2.0%. The lowest federal tax bracket is 14% for 2026 and subsequent years.” — CRA T4032 Payroll Deductions Tables, January 2026

Understanding your bracket position is one piece of a broader financial health picture. Alongside tax planning, building strong credit can expand the financial tools available to you. WideJournal’s guide on how to improve your credit score covers practical steps that complement smart tax management.

Financial Disclaimer: This article is for informational purposes only and does not constitute financial, investment, or tax advice. Always consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.

Frequently Asked Questions

What is the standard deduction for 2026 in the US?

According to the IRS, the 2026 standard deduction is $16,100 for single filers, $32,200 for married couples filing jointly, and $24,200 for heads of household. These amounts reflect adjustments under the One Big Beautiful Bill Act and annual inflation indexing confirmed in Revenue Procedure 2025-32.

What is Canada’s lowest federal tax rate in 2026?

Canada’s lowest federal income tax rate is 14% for 2026 and subsequent years. The CRA T4032 Payroll Deductions Tables for January 2026 confirm this rate, which took effect July 1, 2025, representing a reduction from the previous 15% bottom rate.

Does the no-tax-on-tips provision apply permanently?

No. The IRS confirms the no-tax-on-tips exclusion is a temporary provision under the OBBBA running from 2025 through 2028 only. It is not a permanent feature of the tax code and will expire unless Congress passes legislation to extend it beyond the 2028 tax year.

How do US and Canadian top federal tax rates compare for 2026?

The US top federal marginal rate is 37%, applying to taxable income above $626,350 for single filers or $751,600 for married filing jointly. Canada’s top federal rate is 33% on income above approximately CAD $246,752. Canadian provincial taxes are separate and push combined marginal rates higher in most provinces.